Introduction to the real estate market in Mallorca

Mallorca, the largest of the Balearic Islands, has become one of the most sought-after locations for real estate investments in recent years. The combination of beautiful beaches, a mild climate and an excellent infrastructure makes the island attractive for both vacationers and permanent residents.

Attractiveness of the real estate market

The real estate market in Mallorca is characterized by high demand and a diverse range of properties. From luxurious villas and historic fincas to modern apartments and traditional townhouses – the island has something to suit every taste and budget. Properties near the coast, in the capital Palma de Mallorca and in exclusive residential areas such as Puerto Andratx or Santa Ponça are particularly popular. Prices vary greatly, with properties in Palma de Mallorca averaging around 4,083 euros per square meter in January 2024, while exclusive locations such as Puerto Andratx have reached prices twice as high at up to 8,687 euros per square meter. The average annual price increase per square meter in Mallorca in 2023 was a full 10.5%, making it the highest increase in property prices in Spain. Demand and activity in the market is high, despite a slight decrease in transactions last year. In 2022, around 8,000 real estate transactions were carried out in Mallorca, while in 2023 there were around 7,000 transactions.

Current trends and developments

In recent years, some remarkable trends have emerged in the Mallorcan real estate market:

- Sustainability: More and more buyers are attaching importance to sustainable construction methods and energy-efficient buildings. Solar systems, water-saving systems and environmentally friendly materials are more in demand than ever. This is reflected in an increase in demand for “green” buildings of around 20% over the last 5 years.

- Renovation projects: Historic properties and fincas that are modernized and renovated enjoy great popularity. These projects often offer the opportunity to combine the charm of traditional architecture with modern living comfort. Renovation costs can range from 500 to 1500 euros per square meter, depending on the scope of the work.

- Exclusive locations: The market for luxury real estate is booming. Exclusive locations with sea views or direct access to the beach are in high demand and fetch high prices. A property in the first sea line can cost up to 20,000 euros per square meter.

- Stable performance: The real estate market in Mallorca has shown stable performance in recent years. Despite economic fluctuations, the island remains a safe haven for investments. The annual increase in value of average real estate prices is 3 to 5 %.

For those interested in buying a property in Mallorca, this market offers numerous opportunities. However, it is important to inform yourself thoroughly and seek professional advice in order to make the right decision. The following article will help you to better understand the different financing options and important aspects of buying a property in Mallorca.

Determine financing requirements

Buying a property in Mallorca is a significant investment that requires careful planning and calculation. To ensure that you are well prepared financially, it is important to determine all financing requirements in advance.

Calculation of the required capital

The first step in determining the financing requirement is to calculate the total capital requirement. This includes not only the purchase price of the property, but also other necessary expenses. The required capital can be calculated using a simple formula:

Required capital = purchase price + ancillary costs + renovation costs

The additional costs include notary fees, land registry fees, estate agent’s commission and land transfer tax. In total, these can account for up to 10-14% of the purchase price. For example, notary fees in Spain are around 0.1 to 1 % of the purchase price, land registry fees are around 0.5 to 1 % and the estate agent’s commission is usually 4 to 6 % of the purchase price. Financing costs should also be taken into account, especially if you are taking out a loan. These include interest and any processing fees.

Purchase price and ancillary costs

In addition to the actual purchase price, you need to calculate the additional costs precisely. Notary fees and land register fees are unavoidable, as the notary plays a central role in processing the property purchase and entry in the land register is required. If you hire an estate agent, you should factor in their commission. The land transfer tax, which in Mallorca is between 8% and 13% of the purchase price, must also be taken into account. If you are buying an older property, additional renovation or conversion costs may be incurred, which should also be planned for from the outset.

By applying the above formula, you can ensure that you realistically record all relevant costs and that your real estate financing in Mallorca is on a solid footing. It is advisable to consult a financial advisor to plan all relevant costs in detail and avoid any financial surprises.

Equity and debt capital

Financing a real estate purchase in Mallorca requires a careful balance between equity and debt. Both financing components play a decisive role in how solid and sustainable your investment is.

Meaning of equity

Equity refers to the amount you invest from your own funds in the purchase of real estate. It has several advantages: Firstly, it reduces the need to take out large amounts of credit, which saves you interest costs. Secondly, a high equity ratio signals to banks and credit institutions that you are financially stable, which increases the likelihood of loan approval and may lead to better conditions.

A high equity ratio can also give you more room for negotiation on the purchase price and strengthen your position vis-à-vis sellers. It is therefore advisable to contribute as much equity as possible to the purchase, ideally at least 30% of the purchase price. This recommendation is based on the fact that Spanish banks generally require a minimum down payment of 20%, but a higher equity ratio often enables better credit conditions. It is important to note that buyers who are resident in Spain must make a minimum deposit of 20%, while foreign buyers must make a minimum deposit of 30%. Therefore, the more equity you have, the better your chances with the bank, especially if you are not resident in Spain.

Borrowing options

Borrowed capital includes all the money you raise through credits or loans to finance the purchase of real estate. There are various options available to you in Spain:

- Mortgage loan: This is the most common form of debt financing. A mortgage loan in Mallorca is secured by the property itself, which means that in the event of a default, the bank has the right to sell the property to pay off the debt. The conditions for mortgage loans vary depending on the bank and personal creditworthiness. It is important to note that non-resident buyers are granted a loan of up to 70% with a maximum term of 20 years, while resident buyers can take out a loan of 80% with a term of 40 years.

|

Non-resident buyers |

Residents |

| Credit size |

Up to 70% |

Up to 80% |

| Minimum down payment |

Up to 30% |

Up to 20% |

| Runtime |

Maximum 20 years |

Maximum 40 years |

- Documents required for a mortgage application in Spain:

- Copy of passport

- NIE number

- Proof of employment or income

- Last income tax return

- A purchase agreement

- A receipt for the payment of property tax

- Complete information on other loans that are currently being serviced

- Proof of your assets and debts

- Copy of the existing title deeds

- Personal loans: In addition to mortgage loans, personal loans can also be an option. These are usually not secured by the property and therefore often have higher interest rates. However, they can be more flexible and can be paid out more quickly.

- Loans from friends or family: In some cases, it may make sense to consider loans from friends or family members. This type of financing can offer more favorable terms and does not require formal applications or credit checks. However, clear agreements should be made to avoid potential conflicts.

- Investment partnerships: Another option is to join forces with other investors. Through a partnership, you can share the financing burden while benefiting from the combined resources and knowledge.

Choosing the right mix of equity and debt capital depends on your individual financial situation and your long-term goals. It is advisable to seek the support of a financial advisor or a specialized real estate consultant to find the optimal financing structure for you. This will ensure that your investment remains viable not only today, but also in the future.

Mortgage loans in Mallorca

A mortgage loan is often the preferred method of financing a property purchase in Mallorca. In order to successfully obtain such a loan, various requirements must be met and it is important to understand the conditions in detail.

Requirements for granting a loan

In order to obtain a mortgage loan in Mallorca, you must meet certain requirements. Banks usually check your creditworthiness, financial situation and the stability of your income. Typical requirements include proof of income that proves your sources of income and their stability, for example through payslips or tax returns. A good credit rating is crucial, which is why banks check your credit history and your ability to service existing debts. A significant amount of equity (ideally at least 30% of the purchase price) is also an advantage. In addition, the bank will carry out a valuation of the property to ensure that the purchase price is reasonable and that the property can serve as collateral.

Interest rates and terms

The conditions of a mortgage loan vary depending on the bank and your individual situation. Two important aspects are the interest rates and the terms. The interest rates for mortgage loans can be fixed or variable. A fixed interest rate remains constant over the entire term of the loan, which gives you more planning security. A variable interest rate, on the other hand, can change based on market conditions. Variable interest rates can potentially be more favorable, but also carry a higher risk. Typical interest rates for mortgage loans are currently around 2 to 3% for fixed rate loans and 1 to 2% for variable rate loans for resident buyers. Non-resident buyers can expect a fixed rate of around 3.9 to 4.2% and a variable rate of around 5.3-5.6%. A major difference to financing through German banks is that the interest rates on Spanish mortgages are often linked to the Euribor. The Euribor (European Interbank Offered Rate) is the interest rate at which European banks lend money to each other. This means that monthly payments can increase if the Euribor rises, which increases the risk of financing.

The term of a mortgage loan can vary greatly, typically between 10 and 30 years. A longer term leads to lower monthly installments, but also to higher overall costs due to the interest incurred. A shorter term means higher monthly payments, but reduces the overall cost of the loan. The way in which you repay your mortgage loan can also vary. The most common repayment type is the annuity loan, where you pay constant monthly installments that include both interest and repayment. At the beginning, the larger part of the installment consists of interest, while the repayment portion increases over time. Another variant is the amortizing loan, where you pay constant repayments, with the interest burden decreasing over time as the remaining debt decreases. This leads to a decreasing total monthly burden. Another, less common option is the bullet loan. Here you only pay the interest during the term and repay the entire loan amount at once at the end of the term. This option is riskier and requires good financial planning.

It is important to compare different offers and choose the best conditions for your situation, taking into account both the monthly burden and the long-term costs. The choice of repayment type depends on your financial situation and personal preferences.

Banks and financial institutions in Mallorca

Choosing the right bank or financial institution is a crucial step in financing your property purchase in Mallorca. Different banks offer different conditions and services, which should be carefully compared.

Mortgage loan provider

There are numerous banks and financial institutions on Mallorca that offer mortgage loans for foreign buyers. These include both Spanish banks and international institutions with branches on the island. Here are some of the main providers:

-

-

- Spanish banks: Local banks such as Banca March, Banco Santander, CaixaBank and Banco Sabadell are established providers with extensive knowledge of the Spanish real estate market. They usually offer a wide range of mortgage loans with different conditions.

- International banks: Banks such as Deutsche Bank, Barclays and HSBC also have branches in Mallorca and offer mortgage loans. These banks can be particularly attractive if you are already a customer in your home country and want to take advantage of an existing relationship.

- Specialized mortgage providers: There are also specialized providers that focus on mortgage loans for foreign buyers. These institutions often have tailor-made offers that meet the specific needs and challenges of international buyers.

Conditions and services

The conditions and services offered by different banks and financial institutions can vary considerably. Here are some important aspects you should consider:

-

-

- Interest rates: The interest rates for mortgage loans can be fixed or variable. A fixed interest rate offers planning security as it remains constant over the entire term of the loan. Variable interest rates can change and potentially be more favorable, but also carry the risk of rising costs.

- Terms: The term of the loan influences the amount of the monthly installments and the total cost of the loan. A longer term leads to lower monthly installments, but higher total costs due to interest. A shorter term reduces the overall costs, but requires higher monthly payments.

- Repayment modalities: Different banks offer different repayment options. The annuity loan, where you pay constant monthly installments, is the most common form. There are also repayment loans, where the repayment installments remain constant and the interest charge decreases over time, as well as bullet loans, where only interest is paid during the term and the entire loan amount is due at the end of the term.

- Special repayments: Check whether the bank allows unscheduled repayments without additional fees. Unscheduled repayments allow you to make unscheduled payments and reduce the loan term and interest costs.

- Services: The quality of customer service and support provided by the bank can also be crucial. Some banks offer comprehensive advisory services, including assistance with legal issues and the valuation of the property.

Tax aspects of buying real estate

When buying a property in Mallorca, it is important to know the tax obligations and burdens. These should not be underestimated and should be taken into account when financing your property in Mallorca. The most important tax aspects include land transfer tax, property tax and income tax on rentals.

Real estate transfer tax and property tax

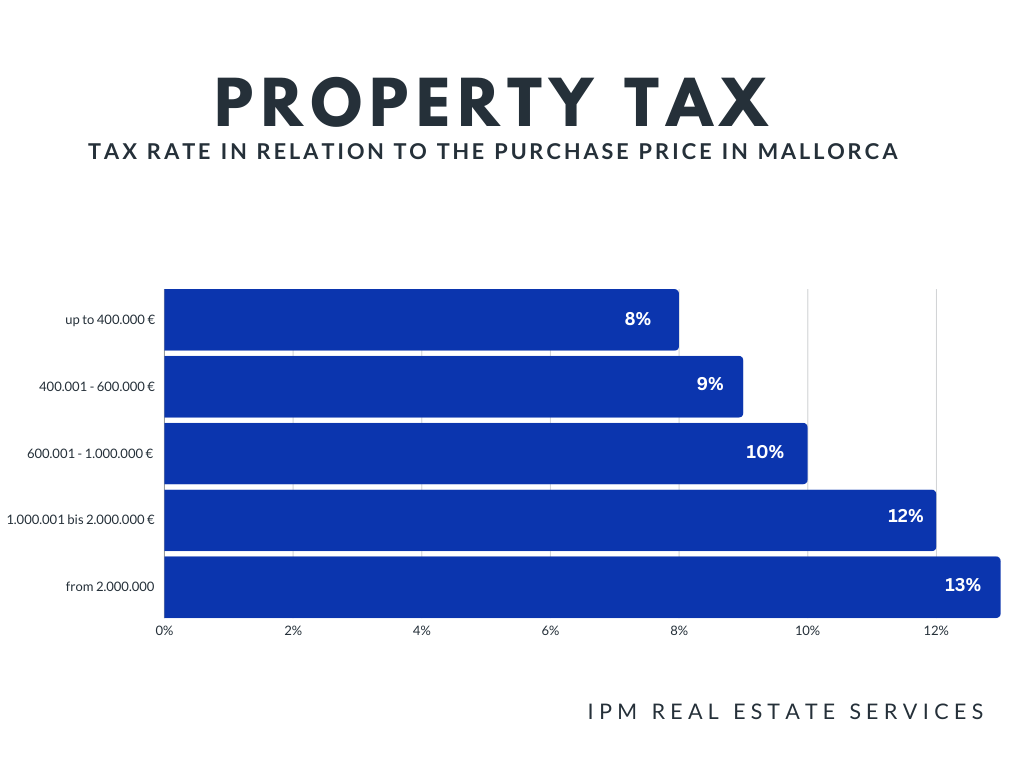

Property transfer tax (Impuesto sobre Transmisiones Patrimoniales) is payable on the purchase of a property and varies depending on the region and purchase price. In Mallorca, the property transfer tax is generally between 8% and 13% of the purchase price. This range depends on the purchase price of the property – for real estate:

-

-

- up to 400,000 euros, the tax rate is 8%

- between 400,001 and 600,000 euros, the tax rate is 9%

- between 600,001 and 1,000,000 euros, the tax rate is 10%

- between 1,000,001 and 2,000,000 euros, the tax rate is 12 %

- from 2,000,001 euros, the tax rate is 13 %

It is important to include this amount in your calculation from the outset, as it is due when the purchase contract is concluded. This tax represents a significant cost factor and should not be underestimated. It is paid directly after the purchase and is a one-off payment.

Property tax (Impuesto sobre Bienes Inmuebles, IBI), on the other hand, is an annual tax levied on the ownership of real estate. The amount of the property tax depends on the cadastral value of the property and the tax rate of the respective municipality. This tax is comparatively low, but it must be paid every year. The exact amounts can vary depending on the location and value of the property, so you should include these regular costs in your long-term budget planning.

Income tax on letting

If you plan to rent out your property, you will have to pay tax on the rental income in Spain. The income tax (Impuesto sobre la Renta de No Residentes, IRNR) for non-residents is currently 24% of the gross income. This means that you cannot make any deductions for expenses such as maintenance or administration costs. This tax liability applies regardless of whether the rental income is earned in Spain or abroad.

It is advisable to plan your tax obligations carefully and, if necessary, consult a tax advisor to ensure that you meet all legal requirements and take advantage of possible tax benefits.

Funding programs and subsidies

When buying a property in Mallorca, state funding programs and regional subsidies can provide valuable support.

State and regional funding

Spain offers various government support programs aimed at facilitating the purchase of property. These programs are often aimed at promoting the purchase of first homes or improving access to housing for certain population groups. For example, there are special loan programs for young buyers or low-income families. These loans are characterized by lower interest rates and more favorable terms, which reduces monthly payments and facilitates access to real estate.

In addition to the state programs, there are also regional subsidies provided by the autonomous communities. These regional subsidies can include grants, tax breaks or particularly favorable loans. They are often linked to certain conditions, such as the obligation to use the property as a main residence for a certain period of time or not to exceed certain income limits.

It is important to find out about the support programs and subsidies available and check whether you are eligible for this support. The combination of state and regional support can make all the difference and make your path to home ownership in Mallorca easier. Plan carefully and use all available resources to get the most out of your property purchase.

Alternative financing options

In addition to traditional mortgage loans, there are a number of alternative financing options that can help you realize the purchase of a property in Mallorca. These options can be particularly attractive if traditional financing methods are not sufficient or additional flexibility is required.

Crowdfunding and building society loans

Crowdfunding is a modern and innovative way of financing real estate. Several investors come together to jointly finance a property. This method can be used for both smaller projects and larger investments. Crowdfunding allows you to gain access to capital without having to rely on a single bank. It also allows you to spread the risk across several shoulders and potentially obtain more favorable conditions. Real estate crowdfunding platforms often offer specialized projects that are well monitored and managed, providing additional security.

Another proven alternative is the building society loan. A building society loan combines savings and a loan in one contract. First, you save a certain amount over a fixed period of time, which is then used as equity for the property purchase. After the savings phase, you receive a low-interest loan which, together with the amount saved, enables you to purchase the property. The advantage of this method is that you have stable and often very favorable interest rates over the entire term. In addition, regular saving encourages disciplined financial planning.

Investment partnerships

Another option for real estate financing in Mallorca is the investment partnership. Here you join forces with one or more partners to acquire a property together. These partnerships can take various forms, such as joint ventures or investment companies. Investment partnerships also offer the advantage that you share the financial burden while benefiting from the combined resources and knowledge of the partners. This structure can be particularly advantageous if you want to realize larger or more complex projects that you could not manage on your own.

In investment partnerships, it is important to make clear contractual agreements to define the rights and obligations of all parties involved. This includes regulations on decision-making, profit distribution and possible exit scenarios. A well-structured partnership can minimize risk while increasing the chances of a successful and profitable investment.

Alternative financing options offer you flexibility and additional ways to realize your dream of owning your own home in Mallorca.

Risk management for real estate acquisitions

If you want to buy a house in Mallorca, you should protect yourself against potential risks. Well thought-out risk management will help you to avoid financial losses and protect your investment. The most important aspects include taking out home insurance and taking currency fluctuations into account.

Residential building insurance

Homeowners insurance is one of the most basic measures you can take to protect your property. This insurance generally covers damage caused by fire, storm, hail, mains water and other natural events. You can also extend your insurance policy to cover burglary, vandalism and other risks. Taking out comprehensive home insurance ensures that you are financially protected in the event of damage and do not have to bear expensive repairs or reconstruction costs alone. For a house of around 100 square meters, you can expect to pay around 350 euros.

Currency fluctuations

If you are a foreign buyer purchasing a property in Mallorca, currency fluctuations are an important factor to consider. Fluctuations in exchange rates can have a significant impact on the total cost of your investment. An unfavorable exchange rate development can result in you having to pay more for your property than originally planned.

Fluctuations in the Euribor and the associated currency fluctuations can be significant and should be carefully considered when planning real estate financing in Mallorca. Historically, the Euribor has ranged from around -0.5% to over 5% over the last decade. These fluctuations depend on European monetary policy, economic developments and other macroeconomic factors.

As a rule of thumb, you can plan for a fluctuation range of around 1% to 2% per year for the Euribor. This means that your mortgage interest rates can rise or fall accordingly, which has a direct impact on your monthly installments.

In addition to Euribor fluctuations, foreign buyers should also take currency fluctuations into account. Exchange rates can vary considerably depending on political events, economic stability and market sentiment. A typical fluctuation range for the euro against other currencies such as the US dollar or the British pound can be around 5% to 10% per year.

It is advisable to build a buffer zone into your budget to compensate for potential interest rate and currency fluctuations. For example, you could plan your financing so that you can cope with an increase in monthly installments of up to 20 % to be on the safe side.

There are various strategies for hedging against currency fluctuations. One option is to conclude a currency forward contract, with which you can secure a fixed exchange rate for a future date. This gives you planning security and protects you against unexpected exchange rate fluctuations. Another strategy is to make your payments in tranches to spread the risk and benefit from favorable exchange rates.

Obtain professional advice

Buying a property in Mallorca is a significant investment that requires careful planning and informed decisions. It is therefore advisable to seek professional advice to ensure that you understand and make the most of all aspects of the property purchase.

Real estate agents and lawyers

An experienced real estate agent can help you find the right property and make the buying process go smoothly. Agents know the local market very well and can give you valuable insights into the best locations, current market trends and realistic prices. They will support you in your search for suitable properties, conduct viewings and negotiate with sellers on your behalf. A good estate agent will ensure that you receive a fair offer and have all the necessary information and documents available and will usually cost you around 4 to 6% of the purchase price.

In addition to a real estate agent, you should consult a lawyer who specializes in Spanish real estate law. A lawyer can help you avoid legal pitfalls and ensure that the purchase contract is correctly worded in your favor. The lawyer will check all relevant documents, such as the land register extract and the purchase contract, and ensure that the property is free of encumbrances and legal problems. He can also help you with the handling of land transfer tax and other legal requirements. The cost of a lawyer is usually around 1% – 1.2% of the purchase price plus VAT.

Conclusion

Buying a property in Mallorca is a significant and often life-changing decision. It requires careful planning, extensive research and the involvement of various professionals to make the process smooth and successful. In this article, we have highlighted the most important aspects of real estate financing in Mallorca, from determining financing needs and the different types of mortgages to tax aspects and alternative financing options.

First of all, it is crucial to determine the total financing requirements, including the purchase price, ancillary costs and any renovation costs. The right mix of equity and borrowed capital plays an important role in creating a solid financial basis.

A sound understanding of mortgage loans, including eligibility requirements, interest rates and terms, is essential. It is worth comparing different offers from banks and financial institutions in Mallorca to find the best conditions. In addition, alternative financing options such as crowdfunding or investment partnerships can be considered.

The tax aspects of buying a property, such as land transfer tax and annual property tax, should also not be forgotten. Good tax planning helps to keep long-term costs under control and avoid potential financial surprises. Funding programs and subsidies offer additional support and can make it easier to purchase a property.

Risk management is another important aspect of protecting your investment. Taking out homeowners insurance and considering currency fluctuations are essential steps to minimize financial losses.

Last but not least, seeking professional advice from real estate agents, lawyers and financial advisors is crucial. These experts provide valuable support and expertise to ensure you make informed decisions and avoid potential pitfalls.

By planning carefully and using all available resources, you can successfully realize the dream of owning your own home in Mallorca. We hope that this article has given you helpful insights and practical tips to help you start your real estate purchase well prepared. Good luck with your project!